As Mark Twain might have said, “The reports of retail’s death are greatly exaggerated.” Indeed, after nearly a decade of massive retail bankruptcies and store closings, lockdowns during the pandemic, and projections of an in-store shopping apocalypse, many industry participants say the horizon is bright for shopping centers and high streets across the world.

To be sure, the landscape has been altered, but the consumer appetite for in-store shopping is robust, and retailers, both legacy and fledgling, are in a feeding frenzy. Store sizes are mostly shrinking while outdoor shopping centers and off-mall locations are getting star treatment, forcing many owners of enclosed malls to rethink game plans. And many already were.

“The narrative that retail was dying because everyone was moving to online shopping – it was just never true,” says Kevin McCrain, chief executive of the US retail division of Brookfield Properties and managing partner in its real estate group.

Online shopping continues to expand, but contrary to what was once popular belief, it is not at the expense of brick-and-mortar retail. The two means of shopping have come to rely on each other.

Moreover, the economic impact on the once struggling sector, exacerbated by the pandemic, higher interest rates and changes in consumer spending, has created opportunities for investors. Retail square footage is shrinking as obsolete centers have disappeared or underwent conversion, and new development has stalled because of higher costs tied to capital and funding, materials and wages.

The supply demand equation

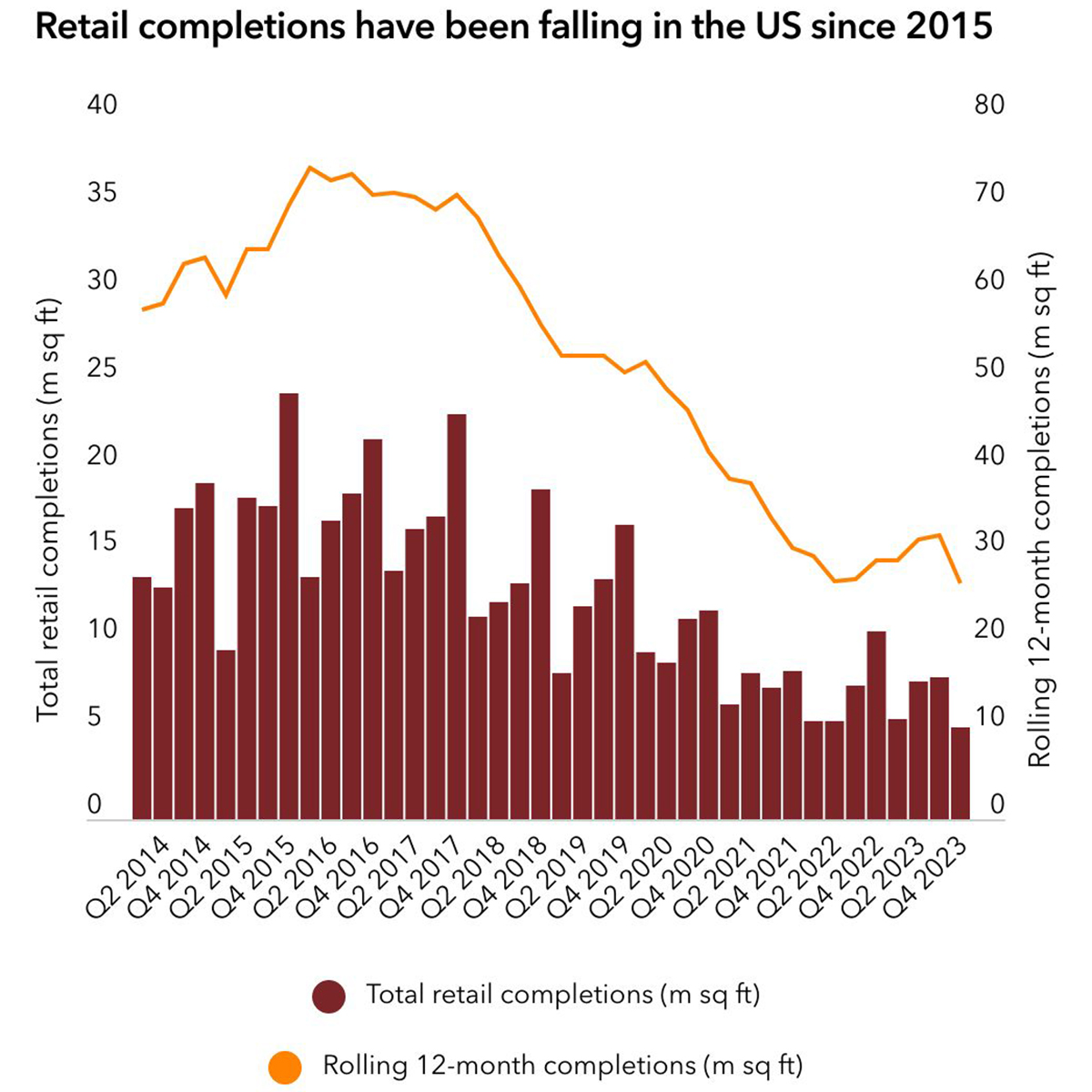

Retail vacancy rates in the US have hit record lows while new retail construction has fallen to the lowest level in decades, making this an interesting time for investment in the sector.

The trick with retail is it has to be kept full, no matter where in the world it is. Empty storefronts are not only unsightly and open invitations for debasement, shoppers tend to walk away from them rather than walking past them. That is especially problematic on high streets and in malls anchored by big-box tenants that have ceased to exist or have substantially trimmed their portfolios, like Sears, Macy’s, Bloomingdale’s, Lord & Taylor, Saks Fifth Avenue, Neiman Marcus and others. Even successful retailers located next to these shuttered stores see traffic drop.

Major store closings and reorganizations were in play a few years ahead of the pandemic, which only exacerbated the situation and prompted the dire prognostications across the sector.

Managers have been aggressively shifting gears by breaking up those big-box spaces into smaller ones or finding other large tenants to occupy them, and have not been short on demand. Discount and off-price retailers, sports retailers, medical centers, distributors, entertainment venues and assorted-sized eateries are taking root.

That is not to say the flight that many national retailers are taking out of malls is anywhere near ending. Location, location, location are the three most important matters for real estate, bolstering neighborhood and grocery-anchored centers and strip malls.

The work-from-home movement has created more shopping opportunities for many suburban consumers, and specialty retailers as well as department and clothing store retailers are following them home, giving rise to more accessible neighborhood shopping centers in densely populated urban and suburban locations.

“The asset class is expected to experience steady performance, with unchanging vacancy rates and moderately positive rent growth for neighborhood and community shopping centers,” Ermengarde Jabir, senior economist at Moody’s Analytics, noted in JPMorgan’s 2024 Commercial Real Estate Outlook.

Grocery-anchored properties have long been the backbone of many neighborhood centers, and for property owners such as PGIM Real Estate, they are remaining center stage. Some 80 percent of PGIM’s 16 million square feet in the US has a grocery component that is increasingly attractive to retailers looking for smaller, off-mall locations that will remain in demand.

That is why shoppers and landlords are seeing smaller versions of stores such as Footlocker, Bath & Body Works and Signet’s Kay Jewelers, Zales and Jared – and even Ikea and Burlington – open in those neighborhood centers.

“At the end of the day, retailers and landlords are working together to make the best shopping experiences by curating a tenant mix that’s convenient and fits that community as best it can,” says Soultana Reigle, head of US equity at PGIM, the asset management arm of American life insurance company Prudential Financial.

Retailers need bricks

While some legacy retailers are still in recovery mode, the trend of younger online retailers opening brick-and-mortar stores is on fire – another movement that is pumping occupancy rates at shopping centers.

“The importance of brick-and-mortar has never been higher,” David Simon, CEO of retail-focused real estate investment trust Simon Property Group, said on a conference call in February. “Don’t get me wrong, e-commerce is critically important, [but] pure online, they run into problems. They really need to be connected to brick-and-mortar for survivability.”

That is called the halo effect, a phenomenon many property owners have embraced with open arms. “When those digitally native brands go into new stores, they see a positive increase in net sales by 14 percent,” says Alison Hallberg, PGIM’s head of US retail asset management. “Even existing tenants like Ulta, when they open new stores in a certain location, online sales go up 7 percent. If they close stores, their online sales go down 11.5 percent.”

Click to enlarge (Source: CBRE Econometric Advisors)

What’s more, deliveries of online sales have become a critical indicator of where to open new stores or relocate smaller versions of traditional shops. Consumers working from home who want to run in and out of a store for online pickups and returns is fueling that expansion. As a result, investors are seeing occupancy rates soar past pre-covid rates, some to record highs in the upper 90s.

“We’re 95 percent leased across our business and retailers continue to expand,” Brookfield’s McCrain says. And at a conference he hosted with some 200 retailers, McCrain adds that they “had more than one say how excited they are about their store’s growth prospects.”

Lifestyle centers forever

Major shopping centers are controlled by a handful of big owners, including Brookfield, Unibail-Rodamco-Westfield, Simon, Taubman, Kimco and others. Many of their major centers are undergoing some sort of renovation.

Brookfield, like many other major shopping center owners, has been in a constant state of redevelopment at large properties such as its Oakbrook Center outside Chicago and Tyson’s Galleria near Washington, DC, where it is stepping up luxury store divisions and adding new entertainment venues.

Click to enlarge (Source: CBRE Econometric Advisors)

Simon Property Group, the largest mall operator in the US, has reconfigured several of its centers after big-box retailers Sears, Macy’s and JC Penney’s went out of business or shuttered hundreds of stores. For example, at the Brea Mall in the foothills of California’s Orange County, Simon is redeveloping what was once a 162,000-square-foot Sears store and Sears Auto into a 119,000-square-foot outdoor plaza attached to 47,000 square feet of shops and restaurants, as well as a 380-unit apartment building. New tenants to Simon’s roster there include Lifetime Fitness, Dick’s Sporting Goods, Untuckit, Zara and Uniqlo, as well as a handful of eateries both large and small.

Paris-based URW is also reinventing malls into 24-hour lifestyle shopping centers such as Westfield Old Orchard in the Chicago suburbs. It is tearing down a three-story, 200,000-square-foot Bloomingdale’s there to make room for 400 luxury apartments with street-level retail and public space. A dark Lord & Taylor store will be converted to house smaller retailers and entertainment spots, including Arhaus, Zara and mini-golf outlet Puttshack.

Income quality conundrum

While the surge of new retailers to the mix is a boon to occupancy, Andrew Allen, global head of research at capital markets firm Savills Investment Management in London, explains that “income quality is less certain” as operational costs climb for property owners who rate contract rents on a percent of retail sales. He worries about sales growth at experiential retailers like axe-throwing and cinemas compared to jewelry or accessory stores.

“How do you make an axe-throwing business more profitable than if you sell handbags? They don’t have that extra dimension that the old retailers have,” Allen notes. “It looks great if you can infill a small space, but the rent density has to be a lower number and you will be less certain about it. That makes the management of shopping centers a much more intense business.”

That is certainly true, but many believe transformations to lifestyle concepts and better-curated shopping experiences will be consumer magnets.

“It’s a question of what are the alternatives,” says Andrew Denye, head of retail at law firm Forsters in London. “If a full conversion away from retail is not an option, or if the scheme does have a strong retail offering, then conversions to ‘lifestyle’ are merely enhancing that.”

The Oakbrook Center shopping mall in Oak Brook, Illinois, features an openair concept, professional landscaping, a park-like setting and upscale tenant roster

Taking on shopping center redos

Brookfield Properties turns a 1960s shopping center into a showstopper for a new era of consumers

Kevin McCrain abhors the retail apocalypse storyline that emerged in 2017 and still haunts the sector. The chief executive of the US retail division of Toronto-based Brookfield Properties admits the commercial real estate sector has experienced some hiccups – covid chief among them – but insists the notion that shoppers did not want to shop in stores was delusional.

“The universal truth is that people like to shop in person,” he says. “In our portfolio of assets, we’ve seen a strong demand for space for some time.”

Brookfield has 158 properties spanning 134 million square feet of retail space. And like most major shopping center owners, it sees occupancy levels collapse when big-box retailers pull out of anchor spaces. But it has been quick to jump in and address the issue.

“The hallmark of a great retail owner is the ability to continually curate your asset and bring in new concepts and new brands and food and beverage additions that will help drive customers and topline sales,” he says.

Oakbrook Center outside Chicago is a prime example of how retail property owners are investing into renovating massive centers. Brookfield began a new multi-million-dollar renovation of the 2.4 million-square-foot center when Sears and Lord & Taylor were closing stores in 2018.

Nestled in suburban Oak Brook, an upscale community outside Chicago, Oakbrook Center has long held a major presence in the town. Brookfield began converting the 1960s-era mall into what it called the “marketplace of the future” with a goal to amass a curated collection of luxury retailers, restaurants, grocery stores and fitness spaces to meet the needs of consumers.

Today, its roster includes Louis Vuitton, Burberry, David Yurman, Gucci, Chanel, RH Mansion, YSL, Vuori, Marc Jacobs, Rolex and Boss, as well as Puttshack and Sony Wonderverse, described as a one-of-a-kind entertainment immersive experience. Anchoring one end of the center is a 164,000-square-foot Lifetime Health Club and Fitness.

“People are rediscovering what it meant to aggregate in common areas and shop, go to restaurants and cinemas,” McCrain says.

It has been a big money maker, according to the owner; the center rings up $1 billion in sales annually. Brookfield refinanced Oakbrook Center last year with a $700 million loan that paid down existing debt of $475 million.

Click here for more from PERE’s 2024 Retail report

Click here for more from PERE’s 2024 Retail report Retailers need bricks

Retailers need bricks

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email:

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email: