This article was sponsored by MSCI

A Google image search for climate change throws up hundreds of photos depicting the damage wrought by extreme weather events like wildfires, hurricanes and flooding – and at the center of these pictures is very often a building.

As well as being on the receiving end of climate change, real estate is also a significant part of the problem. The International Energy Agency (IEA) estimates that the sector contributes over 30 percent of global emissions. As an investment asset class, however, it represents only 9 percent of institutional portfolios. In that sense, it seems private real estate is punching above its weight as a contributing factor to climate change, but being a big part of the problem also means it is a big part of the potential solution. The sense that real estate is punching above its weight may be overstated, however. Some of this is driven by the difference between real estate as a segment of the economy versus real estate as an investment asset class.

Investor vs occupier perspectives

A lot of real estate is held outside of institutional investment portfolios. A huge amount of residential real estate, for example, is owner-occupied or owned by public bodies for social housing purposes, although much is owned by private investors too. Whoever owns it, climate change impacts both property owners and occupiers, but in different ways.

Occupiers are interested in how the impacts of climate change on the physical asset could affect the revenues and costs associated with their operations at a particular facility. Investors and managers are interested in how climate change impacts asset valuations and the financial costs associated with any damage caused to the asset. They are also interested in the costs associated with carbon reduction commitments driven by public policy and by institutional investors themselves.

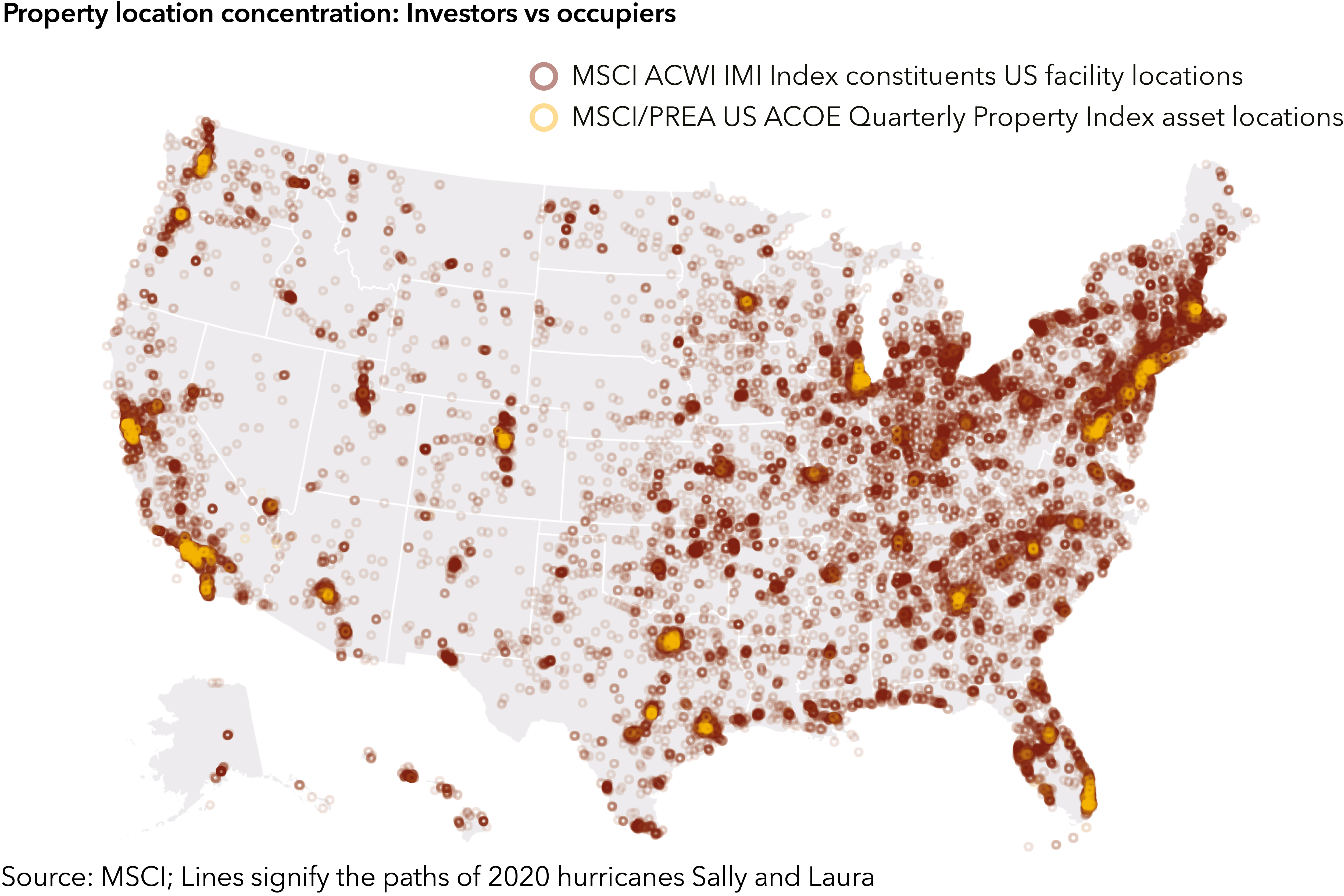

The properties held in open-ended core private real estate funds managed on behalf of institutional investors, like pension funds, are far more concentrated in major cities in the US, as shown in the property location concentration heat map, whereas the facilities used by companies – the owner-occupiers – are more broadly spread across the country, albeit still with greater density in the major cities. The differing geographical spreads of assets drive significant differences in aggregate physical climate risk. So, when thinking about climate risk to private real estate investment portfolios, the physical hazards associated with the cities where they hold more assets drive the risk levels.

Put the emphasis on the ‘change’ in climate change

Extreme weather events seem to occupy an ever-greater share of column inches and air-time in the media these days. This is possibly a function of increasing frequency and intensity of such events but also the collective realization of the link between these events and the ‘climate emergency’ we now face and know is linked to excessive carbon emissions.

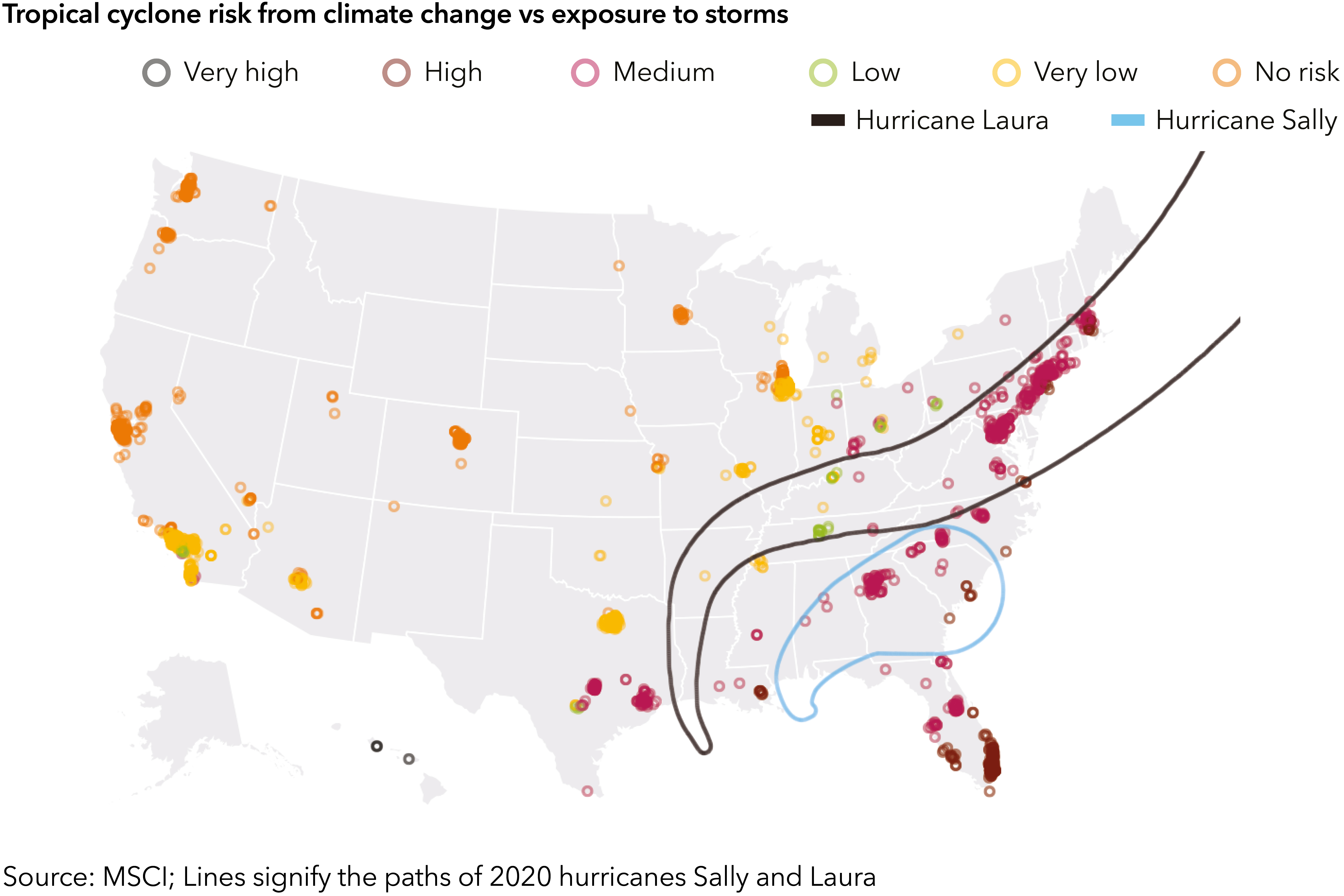

It is natural for investors to devote a lot of time and energy to understanding their portfolios’ current exposure to these kinds of events. It is, for example, a trivial exercise to use publicly available projections of hurricane paths to determine which assets may stand in the way of a storm. Summary statistics of the value and type of assets exposed are easily calculated to describe current exposure.

Take the predicted paths of two recent hurricanes – Hurricane Laura, which swept from the Gulf of Mexico, north-east toward New York, and Hurricane Sally, which passed over land to the south-west of Laura’s path. The quantum and value of property in Laura’s predicted wake was far higher than that of Sally. This is because the properties in Laura’s path were dominated by office buildings whereas Sally was predicted to touch relatively few because its western route drifted to the south of New York rather than passing straight over the city.

However, this analysis, while interesting, says nothing of climate change risk. If we are to understand the physical risk from climate change, we need to understand first how climate change is going to alter the frequency and intensity of such weather events. Then we need to understand the potential financial costs associated with these predicted changes. Finally, we should understand the materiality of these future costs when discounted and compared with assets’ current market value. Calculating such metrics allows the analysis to be seamlessly incorporated in to broader financial and risk analysis.

Translating risk measurement into risk management

Properly understanding investors’ current and future exposure to climate risk is only the first step. It begs the question; ‘What can investors do about it?’ Once measured carefully, step by step, it becomes clear that the variety of climate risks plays out very differently across a portfolio and so optimal management techniques may vary by type of risk and portfolio.

Consider a hypothetical portfolio constructed from assets spanning two metro areas – South Florida and New York. If we focus on just two physical climate hazards, coastal flooding and tropical cyclones, we can understand the potential capital value at risk from these hazards as a result of modeled climate change scenarios. Both metro areas are at more risk form tropical cyclones than from coastal flooding. However, if we treat both areas as one portfolio, aggregating the expected value at risk for the worst affected 5 percent of assets for each hazard, it becomes clear the risks are spread very differently across the portfolio.

Although coastal flooding is less impactful in aggregate, nearly all the risk is driven by the worst affected 5 percent of assets. This risk hits very few assets but in a very significant way. Managing this risk may be best achieved by stock picking or asset-level flood defenses.

Tropical cyclone risk is much more significant in aggregate, but evenly spread across the portfolio. Many assets in the portfolio are impacted, but each in a less significant way than for those hit by coastal flooding. Management of this risk may best be achieved through market selection.

An expansive and sophisticated solution required

Understanding climate change risk in the context of real estate is complex and requires a detailed step-by-step modeling process. But climate change is not just a real estate issue; it is a significant threat affecting all areas of life and society. So, simply finding and implementing real estate-specific solutions to address the problem will not be effective if they operate in a bubble. Rather, a coherent, multi-asset class solution is required that will facilitate the optimal allocation of capital across and within asset classes. Such an approach will hopefully help to mitigate climate change and protect investors’ capital – and society more broadly – from the worst of its risks.

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email:

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email: