Investors need to consider multiple drivers when thinking about demand for digital assets in the region, writes Brigg Macadam’s emerging market banker and ADIA’s former real estate global chief operating officer Martin Schwarzburg.

There is a well-known African proverb: “You do not beat a drum with one finger.” This certainly chimes when it comes to factors driving data volume growth rates in sub-Saharan Africa and the associated demand for digital assets like data centers and mobile towers, as there is no one factor responsible.

Martin Schwartzburg

Rather, three drivers have emerged: rapid urbanization, the demographic dividend and data localization and sovereignty.

Rapid urbanization

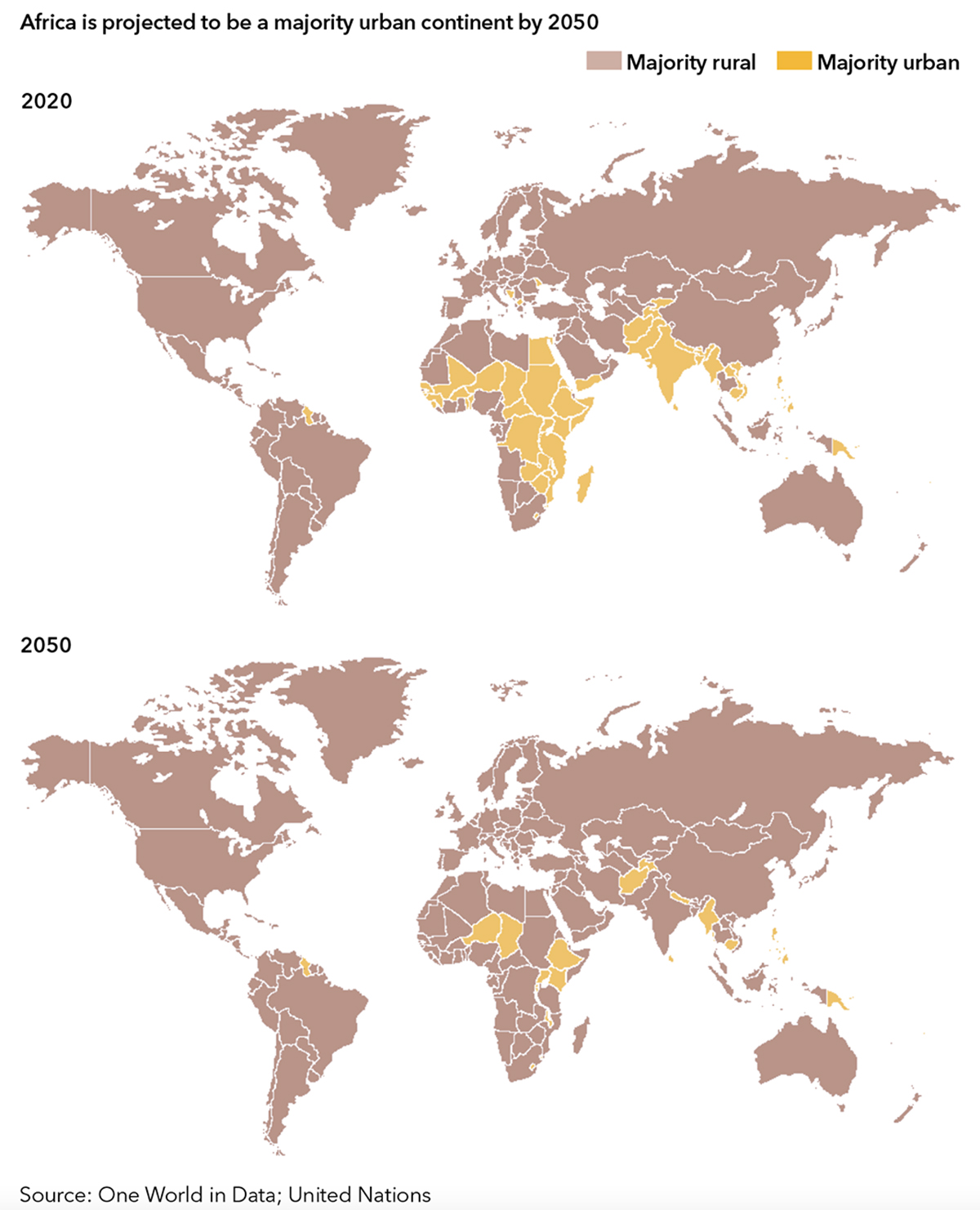

SSA is poised to catch up with the rest of the world over the next 30 years in terms of urbanization levels. In 2020, most of the African continent was majority rural, according to UN data, but by 2050, with the exception of a handful of countries including Ethiopia and Kenya, it is predicted to be majority urban.

While urbanization resulting in increased population density is not without its challenges, especially in emerging markets, it also harbors significant benefits: increased proximity, enhanced connectivity, skills clustering and specialization. These benefits are closely related to productivity gains reflected in increased GDP per capita ratios.

Click map to view full size

This is supported by World Bank data showing China’s development from 1990, when the country had a population density of 120.92 people per kilometer and a GDP per capita of $1,526. By 2017, the population density had increased to 147.67 people per kilometer and GDP per capita to $15,309. This period of rapid urbanization for China could indicate the economic growth potential for a rapidly urbanizing SSA.

Another aspect that deserves consideration is the crucial link between economic growth due to urbanization and the growth of cloud data traffic through cell phone adoption, and hence demand for digital assets like data centers and mobile towers. World Bank data again supports this correlation for the 10 most populous countries in SSA. Ghana, for example, in 1990 had zero mobile cellular subscriptions per 100 people and GDP per capita of $1,920. By 2017, subscriptions had increased to 127.46 and in tandem, GDP per capita rose to $4,228. While data traffic per smartphone will still lag behind regions like China, North America and Europe, where there will be rapidly expanding 5G mobile data traffic, the growth rates across SSA are highlighting the potential.

The demographic dividend

The second driver for data volumes are demographics. The much-debated divergence of SSA’s demographic path compared with almost any other region in the world will, no doubt, put a strain on societies and resources. However, it will also provide the region with a unique growth engine, as younger people tend to have an increased geographic mobility combined with higher adoption rates in terms of digital services and products.

UN data tells the story of that dramatic demographic shift over the next 30 years. By 2050, SSA is projected to have the youngest population in the world, with a median age in the 20-30 range. Contrast that with China and the US, which are expected to have a median age of 48 and 42, respectively.

Data localization and sovereignty

The third major category driving data volumes is the proliferation of complex cloud computing applications, requiring localized data storage to provide an appropriate service quality.

A somewhat related regulatory issue driving the data center demand in SSA is legislation surrounding data protection, comparable to the EU’s General Data Protection Regulation. While not uniform (yet) like in Europe, the lay of the land is clearly recognizable. Legislators in countries like South Africa, Angola and Ghana have already put cross-border data transfer restrictions in place, with others surely to follow their lead. This along with the other factors discussed above will be the ultimate driver for local or regional – for example, the African Continental Free Trade Area – data center demand.

Impact on SSA’s data center sector

Albeit starting from a relatively low base, the SSA data center market is already undergoing exponential growth, and this is catching the eyes of major operators and investors. However, an even more compelling investment case emerges when considering a well-substantiated recent data center supply gap analysis prepared by the Africa Data Centers Association, an industry group, and XALAM Analytics.

Drawing on a broad set of demand drivers, including the ones discussed above, and using India and South Africa as low and mid-range benchmarks, the analysis arrives at a current supply gap of between 54 and 200 data centers for the 10 largest countries in SSA alone. This, of course, is closely linked to stable energy supply as the key ingredient of a data center operation in markets challenged by frequent load shedding.

It is clearly time for more investors to step up to capture the opportunities in the SSA digital space, or, to use another African proverb: “If the rhythm of the drum beat changes, the dance step must adapt.”

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email:

If you do not receive this within five minutes, please try to sign in again. If the problem persists, please email: